|

|

Individual Retirement Accounts (IRAs) are some of the most popular retirement plans available to supplement your retirement years with additional funding. One of the reasons for their popularity is that IRAs are tax-deferred investing tools which can encompass a range of financial products, including stocks, bonds, ETFs, and mutual funds.

Unlike other retirement products, anyone can have one or more IRAs in addition to any other type of retirement account. You can open different kinds of IRAs with a variety of organizations. You can open an IRA at a bank or other financial institution or with a mutual fund or life insurance company or your stockbroker.

|

|

|

|

|

There are several types of IRAs: the traditional IRA, the Roth IRA, SEP, and SIMPLE IRA. Individual taxpayers establish traditional and Roth IRAs, while small-business owners and self-employed individuals establish SEP and SIMPLE IRAs. Any IRA must meet Internal Revenue Code requirements.

When if comes to traditional IRAs, you must know there are limits and other rules that affect the amount that can be contributed to the accounts.

For 2020, your total contributions to all of your traditional and Roth IRAs cannot be more than:

|

|

- $6,000 ($7,000 if you're age 50 or older), or

- your taxable compensation for the year,

if your compensation was less than this dollar limit.

|

|

For 2019, the limits are the same as 2020.

For 2018, 2017, 2016 and 2015, your annual total contributions to all of your traditional and Roth IRAs cannot be more than: $5,500 ($6,500 if you're age 50 or older), or your taxable compensation for the year, if your compensation was less than this dollar limit.

The IRA contribution limit does not apply to rollover contributions and qualified reservist repayments. |

|

|

|

|

| There are two tax advantages of an IRA: |

|

- Contributions you make to an IRA may be fully or partially deductible, depending on which type of IRA you have and on your circumstances; and

- Generally, amounts in your IRA (including earnings and gains) aren’t taxed until distributed. In some cases, amounts aren’t taxed at all if distributed according to the rules.

|

|

Roth IRA contributions are not deductible as they grow tax free throughout your career and beyond, and unlike many other types of retirement accounts, you don't pay any tax when you take withdrawals from a Roth IRA in retirement.

Contributions on your behalf to a traditional IRA reduce your limit for contributions to a Roth IRA. Generally, your filing status has no effect on the amount of allowable contributions to your traditional IRA.

If contributions to your IRA for a year were more than the limit, you can apply the excess contribution in one year to a later year if the contributions for that later year are less than the maximum allowed for that year. However, a penalty or additional tax may apply.

If contributions to your traditional IRA for a year were less than the limit, you cannot contribute more after the due date of your return for that year to make up the difference.

Contributions can be made to your traditional IRA for a year at any time during the year or by the due date for filing your return for that year, not including extensions. You don’t have to contribute to your traditional IRA for every tax year, even if you can. Because the due date for filing federal income tax returns this year has been postponed to July 15, the deadline for making contributions to your IRA for 2019 is also extended to July 15, 2020.

|

|

|

|

As mentioned above, your IRA contributions may be tax-deductible. The deduction may be limited if you or your spouse is covered by a retirement plan at work and your income exceeds certain levels of the modified adjusted gross income (MAGI). The adjusted gross income (AGI) represents your taxable income and is an important figure for your tax return. MAGI represents your comprehensive earnings, including those items that are not taxable, and is used to determine whether an individual qualifies for certain tax benefits.

Your deductible contribution amount begins to phase out when your MAGI rises above a certain amount, and is eliminated altogether when it reaches a higher amount. These amounts vary depending on your filing status.

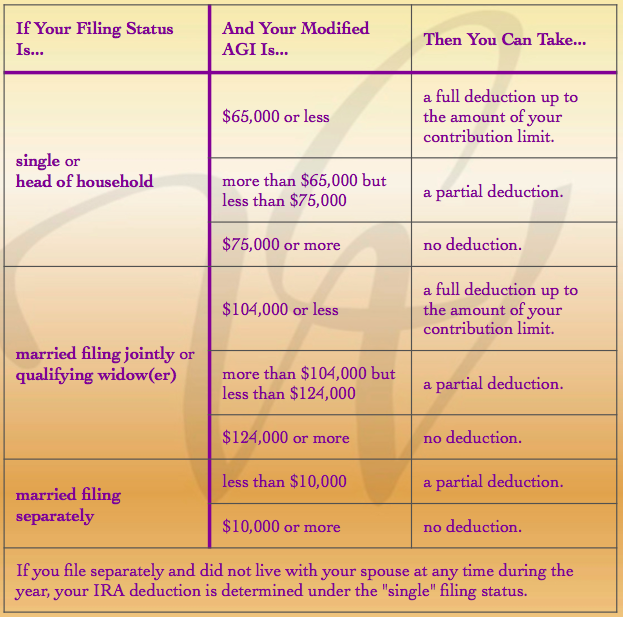

If you are covered by a retirement plan at work, use this table to determine if your MAGI affects the amount of your deduction.

|

|

|

|

|

|

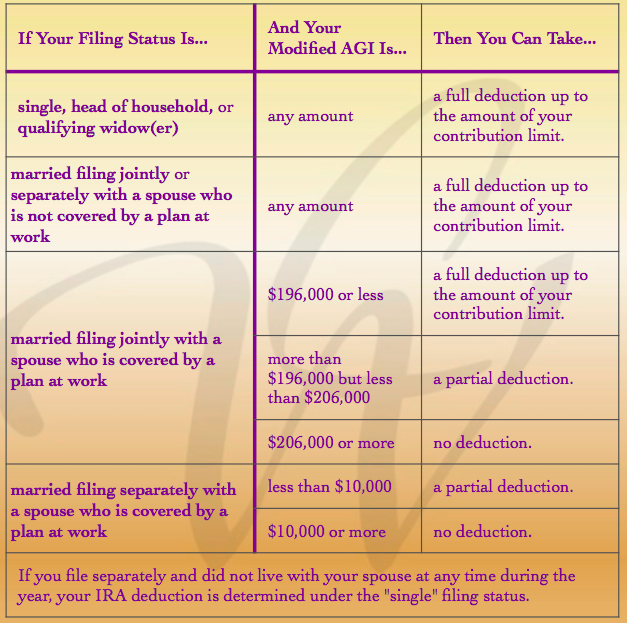

If you are not covered by a retirement plan at work, use this table to determine if your modified AGI affects the amount of your deduction.

|

|

|

|

|

There is a lot more to be said about the IRAs contributions and you should check Publication 590-A, Contributions to Individual Retirement Arrangements, and Publication 590-B, Distributions from Individual Retirement Arrangements, which deal with all kinds of details including: setting up an IRA, contributing to an IRA, transferring money or property to and from an IRA, handling an inherited IRA, receiving distributions (making withdrawals) from an IRA, taking a credit for contributions to an IRA, or make a comparison of traditional and Roth IRAs.

Whether you check the IRS publications or not, you may want to contact a tax advisor to comply with this complicated area of the tax law, and keep up with our newsletters for regular updates on topics of general interest.

|

|

|

|

|

|

|

|