The maximum credit is $1,000 for single filers or individuals and $2,000 for married couples.

Starting in 2018, ABLE account beneficiaries can qualify for the Saver’s Credit based on contributions they make to their ABLE accounts.

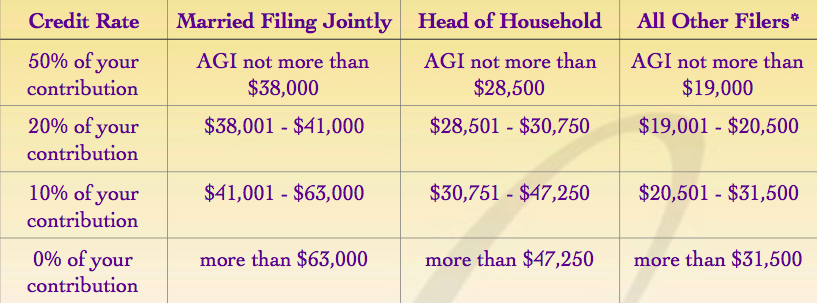

Depending on your income and filing status, you may claim this credit on your return for a percentage of the contributions you made to a qualified retirement plan.

The amount of the credit is 50%, 20% or 10% of your retirement plan or IRA contributions of up to $2,000 ($4,000 if married filing jointly), depending on your adjusted gross income (reported on your Form 1040 or 1040A).

Here are the 2018 figures for the Saver’s Credit: |

|

|

|

|

* All other filers include single, married filing separately,

or qualifying widow(er).

|

|

| The Saver’s Credit can be claimed on Form 8880, Credit for Qualified Retirement Savings Contributions, which will be revised later this year to reflect changes made by the new law. This credit can reduce the amount of tax a person owes or increase their refund. |

|

|

|

|

In addition to changes made to the ABLE accounts and the Saver’s Credit in favor of eligible individuals with disabilities, some funds now may be rolled into an ABLE account from the designated beneficiary’s own 529 plan or from the 529 plan of certain family members.

A 529 plan is a college savings plan sponsored by a state or educational institution, with tax advantages and potentially other incentives to make it easier to save for college and other post-secondary training, or for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school for a designated beneficiary, such as a child or grandchild.

With a typical 529 plan, earnings are not subject to federal tax and generally not subject to state tax when used for the qualified education expenses of the designated beneficiary, such as tuition, fees, books, as well as room and board at an eligible education institution and tuition at elementary or secondary schools.

Contributions to a 529 plan, however, are not deductible.

As of 2018, the term “qualified higher education expense” includes up to $10,000 in annual expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school.

More details about all changes made to the 529 plans as of 2018 will certainly follow some time during the year. |

|

|

|

|

|

| We think you have more than enough reasons, particularly this year, to keep up with our newsletters and dedicate a little of your time to finding out all the pieces of information which may shape your next tax return. |