|

|

|

|

|

|

|

|

|

|

|

|

Troubles viewing this message? View in browser online here

|

|

|

|

|

Income Tax Withholding Rules

Update 2020

|

|

|

March 03, 2020

|

|

|

|

TCJA permanently modified the wage withholding rules and, replaced “withholding exemptions” with a “withholding allowance, prorated to the payroll period.”

The Form W-4 is also redesigned to make it easier for employees with more than one job at the same time or married employees who file jointly with their working spouses to withhold the proper amount of tax.

In addition, employees can choose to have itemized deductions, the child tax credit, and other tax benefits reflected in their withholding for the year.

As in the past, employees can choose to have an employer withhold a flat-dollar extra amount each pay period to cover, for example, income they receive from other sources that is not subject to withholding.

Under the proposed regulations, employees now also have the option to request that employers withhold additional tax by reporting income from other sources not subject to withholding on the Form W-4.

The proposed regulations permit employees to use the new IRS Tax Withholding Estimator to help them accurately fill out Form W-4.

As in the past, taxpayers may use the worksheets in the instructions to Form W-4 and in Publication 505, Tax Withholding and Estimated Tax, to assist them in filling out this form correctly. You should know that, for the time being, Publication 505 is being revised to reflect legislation enacted on December 20, 2019.

The proposed regulations also address a variety of other income tax withholding issues. For example, they provide flexibility in how employees who fail to furnish Forms W-4 should be treated. Starting in 2020, employers must treat new employees who fail to furnish a properly completed Form W-4 as single and withhold using the standard deduction and no other adjustments. Before 2020, employers in this situation were required to withhold as if the employee was single and claiming zero allowances.

|

|

|

|

|

In addition, the proposed regulations provide rules on when employees must furnish a new Form W-4 for changed circumstances, update the regulations for the lock-in letter program, and eliminate the combined income tax and FICA (Social Security and Medicare) tax withholding tables.

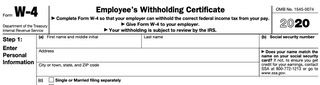

The 2020 Form W-4 contains 5 steps. Every 2020 Form W-4 employers receive from an employee should show a completed Step 1 which includes name, address, social security number, and filing status, and a dated signature on Step 5. Employees will complete Steps 2, 3, and/or 4 only if relevant to their personal situations.

Steps 2, 3, and 4 show adjustments that will affect withholding calculations. Step 2 may be used if you have more than one job at the same time, or are married filing jointly and you and your spouse both work. Step 3 provides instructions for determining the amount of the child tax credit and the credit for other dependents that you may be able to claim when you file your tax return. Step 4 is used to enter the total of your other estimated income for the year, if any (not including income from any jobs or self-employment).

If you want to make sure you are taking the right decisions in all your dealings with the IRS, and especially so when new rules are in place, help from a tax professional is a must.

If you want to stay up-to-date with any relevant news concerning your taxes, then don’t miss out on our weekly newsletters.

|

|

|

|

|

|

|

|

|

In the U.S. tax history, tax withholding is a relatively new concept, the system having been fully and permanently implemented only after the World War Two. Since then, there have been numerous changes and revisions, but the general rule for everybody is that at least 90% of taxes owed is either withheld on each paycheck or paid in estimated taxes throughout the year.

The U.S. income tax is a pay-as-you-go tax, and there are two ways to pay as you go: withholding and estimated tax. Under today's tax withholding system, taxes are collected at the source, meaning that wage earners never see the money that they owe in taxes, it’s taken out of their paychecks and transmitted directly to the federal government by their employers.

|

|

|

|

|

|

Independent contractors aren't subject to withholding, and neither is the income earned by investors, but individuals are responsible for calculating and remitting their own tax payments on a quarterly basis.

The federal withholding system provides the model that 41 states use to withhold state income taxes. Nine states: Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming don't have a state income tax.

For employees, withholding is the amount of federal income tax withheld from your paycheck. The amount of income tax your employer withholds from your regular pay depends on two things:

|

|

- The amount you earn.

- The information you give your employer on Form W–4.

|

|

The U.S. Department of the Treasury and the Internal Revenue Service have recently issued proposed regulations updating the federal income tax withholding rules to reflect changes made by the Tax Cuts and Jobs Act (TCJA) and other legislation.

In general, the proposed regulations, available now in the Federal Register, are meant to accommodate the redesigned Form W-4, Employee's Withholding Certificate, to be used starting in 2020, and the related tables and computational procedures in Publication 15-T, Federal Income Tax Withholding Methods.

The proposed regulations and related guidance do not require employees to furnish a new Form W-4 solely because of the redesign of the Form W-4. Employees who have a Form W-4 on file with their employer from years prior to 2020 generally will continue to have their withholding determined based on that form.

|

|

|

|

|

To assist with computation of income tax withholding, the redesigned Form W-4 no longer uses an employee's marital status and withholding allowances, which were tied to the value of the personal exemption. Due to TCJA changes, employees can no longer claim personal exemptions. Instead, income tax withholding using the redesigned Form W-4 will generally be based on the employee's expected filing status and standard deduction for the year.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

www.carlwatts.com

|

office@carlwatts.com

|

Washington DC

|

Phone: 202 350-9002

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|